WeWork & Airbnb will be Fine

The disruptors of office and lodging are seeing the world reborn in their image.

A century ago, in October 2019, I wrote about why I was optimistic about WeWork and pessimistic about Airbnb. I argued that WeWork had better odds of surviving than was commonly assumed. And that Airbnb was more vulnerable than it seemed.

Almost a year later, I would like to update my position. My optimistic assumptions about WeWork have come true. This does not mean the company is no longer at risk. My pessimistic assumptions about Airbnb have also come true. But I am more optimistic about the company than I was a year ago.

Reading this week’s news made me think of these two companies, and how they can flourish in a post-COVID world. Let’s start with the news.

Until we meet again

Facebook announced that it would allow employees to work from home until July 2021. This means employees will spend a total of 14 consecutive months away from the office. Google and Uber announced similar policies.

In May, I wrote that Landlords are Zucked, following Facebook’s earlier announcement of plans to transition 50% of its workforce to remote over the next ten years. Things seem to be moving faster than planned.

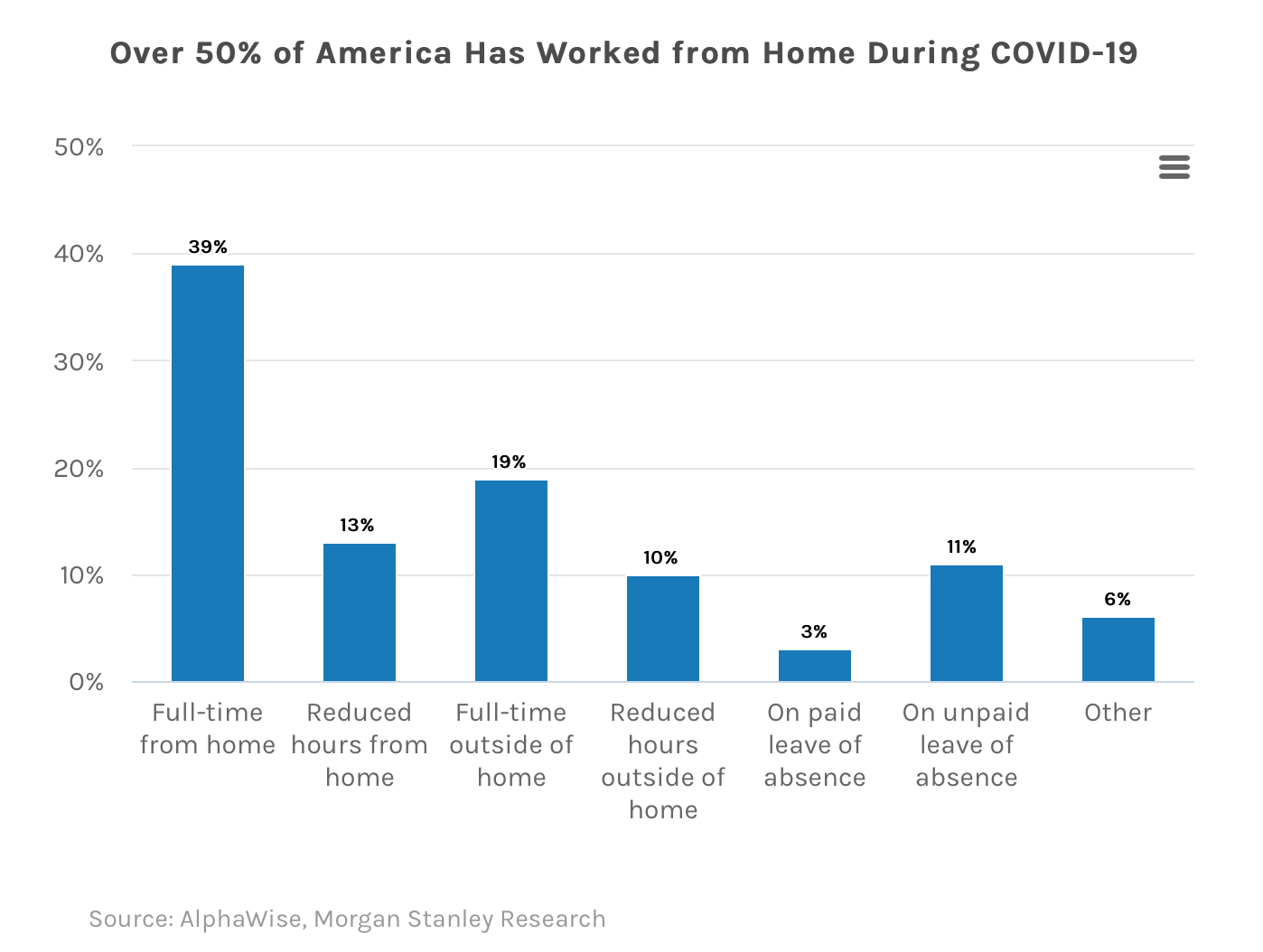

According to HBR and Morgan Stanley, the share of Americans working from home jumped from as low as 5% pre-COVID to 50% by April 2020. While many of these people will, one day, return to the office full time, many others won’t.

The current experiment with remote work is no longer a short break in the usual order of things. After 14 months, you don’t merely lace your shoes and go back to doing whatever you were doing before. Absence does make the heart grow fonder, but only for those who were already in love prior to separation.

How many people were in love with their office?

Uneven City

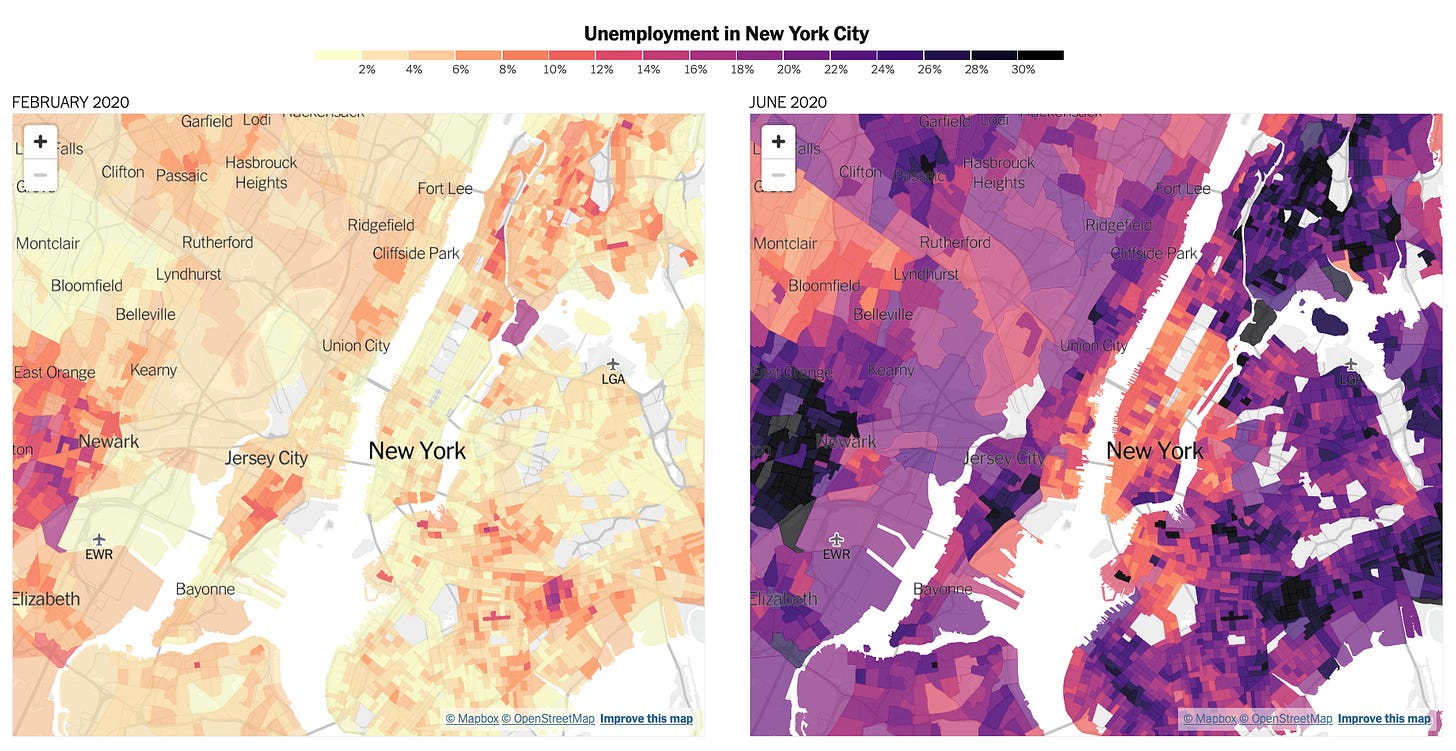

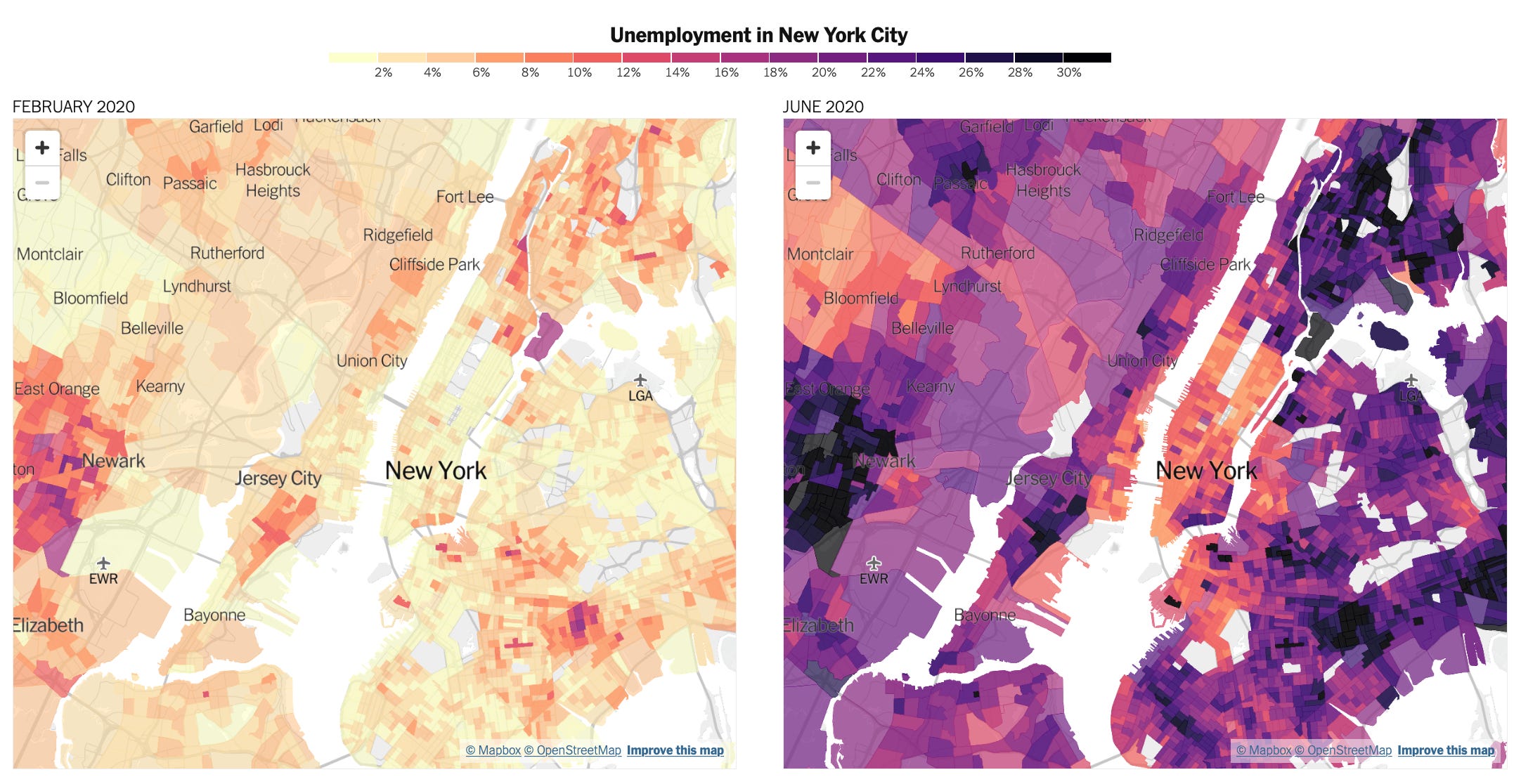

While many can work from home during COVID, many more cannot work at all. The New York Times has a series of visualizations of the virus’s economic impact on the center of the universe.

{kind=link}

Most of Manhattan and the wealthier parts of Brooklyn are doing relatively well. Meanwhile, unemployment rates in other parts of the city are as high as 30%. “It’s as if parts of the Bronx were experiencing the Great Depression while the Upper East Side faced only modest drops in employment.” There are indications that San Francisco is going through something similar.

{kind=link}

Things are even worse than they seem: Many people who are not experiencing the Great Depression are the ones who moved, temporarily, out of the largest cities. Many of these people can also stay away indefinitely. In other words: prosperity can move out of cities, but the depression will stay put.

Follow the Money

It’s easy to assume that most of these people will return to New York or San Francisco once this virus is finished. But the crisis made many people realize that the “big city bargain” no longer makes sense.

Bloomberg published a detailed breakdown of the economics of remote work. The whole thing is worth reading, but one point stood out:

“a typical home [in SF Bay Area] is more than 1,100% of the average skilled worker’s annual salary, far more than the U.S. average of about 340%... Even if a person took a significant pay cut by moving out of the city, they might have more discretionary income in the end. “

Put differently, people move to these cities in search of better-paying jobs. But it is now possible to access high (if not highest) salaries from almost anywhere, and definitely from smaller cities that have been heating up over the past few years (Say, Austin and Denver in the US and Manchester and Birmingham in the UK).

Something in the basic formula is broken. The only way to afford to live in NYC is to work in NYC, but if you don’t have to work in NYC, you don’t need to afford to live in NYC. I experienced this firsthand.

Yes, NYC has all sorts of cool things that are priceless. But many other places do as well. And these places are nipping at NYC’s heels. The city does not have to become worse to lose out; if it remains great — which is in doubt at this point — the fact that people suddenly have more choice means many of them will choose to go elsewhere.

That last point is based on Christensen’s theory: Disruptive competitors are alwaysworse than existing leaders when judged based on existing features and metrics. Nokia was a better phone than the iPhone; Blackberry was a better messaging tool than the iPhone. But the iPhone was good enough as a phone and a messaging tool and much better at all sorts of new things that customers suddenly cared more about — listening to music, taking selfies, playing games. These things seemed frivolous and unproductive — just like having a backyard, or living near a lake, or having a pet goat. But they still won over.

Which brings us back to two companies who grew quickly by offering “terrible” products to people who were hungry for something different. But before that, let’s take a detour through the farm.

Ducking a Meteor

The world is losing its taste for meat. Meat production and estimated consumption dropped in 2019 and is projected by the UN Food & Organization (FAO) to decline again in 2020. Last year was the second time since 1961 in which production fell. A decline for two consecutive years might be indicating a lasting change.

Anecdotal evidence of a broader change is everywhere. Elite athletes from Novak Djokovic to Kyrie Irving are relying on plant-based diets. Burger King and Walmart are now offering faux meat from Impossible Burgers and Beyond Meat. And technologies that “grow” real meat in a lab are starting to churn out products that humans might be willing to eat.

The meat industry takes up a lot of land. According to FAO, “twenty-six percent of the Planet’s ice-free land is used for livestock grazing, and 33 percent of croplands are used for livestock feed production”. A decline in meat consumption would free up a lot of land. It would also force a lot of farms and farmers to come up with new ways to make money.

Some farmers are already diversifying their income. As the New York Times reports, a new batch of "farmer-influencers" earns more from streaming their lives on YouTube than they do from selling animals and animal-produce. The piece follows Morgan Gold, a small-time farmer who figured out how to turn his daily routine into cash, online:

Farmers here struggle to eke out a living from a rocky, uneven soil and hostile climate, and they are astounded — in some cases a little jealous — to discover that Mr. Gold is internet famous, he said.

“He’s found a way to way to monetize farming with less physical labor,” Mr. Galinat said. “Some guys are like, this is silly, since he’s farming 20 ducks. But at the same time, he’s making more than other farmers who have 500 acres of land.”

As one of Mr. Gold’s disciples points out, “He has taught me I am no longer selling hay, I am selling a lifestyle.” For the audience, getting a taste of the lifestyle on YouTube might be a gateway drug to spending more time on an actual farm.

I suspect that a sizable minority of those who don’t have to live in the city will want to spend a few months a year on a farm somewhere. With more land becoming available, and farmers pivoting to hospitality and entertainment, this would be an interesting trend to watch. People will not become farmers, but they would want to experience the lifestyle, now and then, perhaps regularly.

Which brings us back to WeWork and Airbnb.

WeWork Listens

Last week, the coworking giant launched “WeWork On Demand,” a new app that allows anyone — not just existing customers — to book a desk or a private room in multiple locations across NYC. A full-day booking costs as little as $25, cheaper than sitting in a cafe for 8 hours and ordering drinks and pastry to avoid getting kicked out.

In doing so, WeWork is following the lead of two radical companies that are dear to my heart, Breather and Spacious. For years, Breather has enabled anyone to book a private office or meeting room in hundreds of locations across the world, at the click of a button, for as short as an hour or as long as a month (and, with a few emails, even two years).

Spacious enabled individuals to book seats in restaurants that were converted to makeshift coworking spaces during workdays. These restaurants would otherwise open only on evenings and weekends, so they were happy to generate extra income during the day. Last year, WeWork acquired Spacious and then shut it down during the aftermath of its non-IPO. Spacious is now reborn as WeWork On Demand, with the addition of Breather-Esque meeting rooms.

This new initiative offers a way for WeWork to monetize existing space and draw in customers who are ready to commit to a full return to the office but still need an occasional place to work or meet. Unlike Spacious’s original focus, the goal is not just to attract freelancers and people who would otherwise sit at a Starbucks; the goal is to offer a solution for large enterprise customers (Amazon, Morgan Stanley) who want to provide their employees the option to access productive spaces near home or, ultimately, anywhere on earth.

Three-and-a-half years ago, I wrote an article titled What Might Kill WeWork?. It was written while WeWork was an unstoppable meteor and pointed out that “the company thrives on a superior understanding of its customers’ needs. But its business model makes it vulnerable.” The article noted that the combination of long-term leases and short-term customers would not end well: “upfront costs coupled with unstable demand from the world’s most fickle consumers. What could possibly go wrong?”

And the risk was only going to intensify. I mentioned that the company would soon be under pressure from companies such as Breather and Spacious that had a leaner cost structure and under and from more traditional landlords who would launch their own flexible offerings.

Apart from keeping an eye on emerging competitors, I recommended that WeWork stop acting like a cult for startups and stop signing leases with landlords. Instead, I advised it to “shift its focus towards an ‘asset-light’ aggregation model or towards larger tenants who sign longer leases.” I also made another recommendation, which I’ll address in a moment.

Of course, WeWork ran ahead and signed tens of billions in leases and became more cult-like. It did start to focus on enterprise clients and landlord partnerships. Still, these efforts were eclipsed by its insatiable appetite for growth at all costs — which meant signing more leases and exacerbating the risk of its original model.

In 2019, the company filed for an initial public offering. It was not the best time, but it could no longer afford to wait: Its investors and executives were itching for a “liquidity event”; the economy was 11 years into a growth cycle that was destined to end soon, and the company needed more cash.

When WeWork published its detailed financials ahead of the IPO, it was clear that there’s a gap between the company’s story and what investors wanted to hear. Looking at the filings, I was more optimistic than some but pointed out that:

- “The Company’s S-1 highlights troubling governance issues and internal dealings. These alone would be a good reason not to invest in the company.”

- The is worth less than half of its stated valuation of $47 billion (it ended up being valued at much less than that).

- While the company’s lease obligations are scary, but leases are much easier to get out of than most people assume.

- WeWork is not a tech company, but it’s still a legitimate business that can one day be profitable.

- An economic downturn would not be good bad for WeWork, but it would be even worse for traditional landlords and expedite the transformation of the overall market.

Perhaps the most important quote from the article is this one:

When the next downturn arrives, WeWork may very well be in a position to renegotiate many of its leases. For most owners, a crisis is not a great time to lose a major tenant.

That’s precisely what happened. A crisis hit. Landlords were on the defensive. WeWork renegotiated or bailed out on many of its leases obligations. And WeWork’s new management says the company is on track to be cash-flow positive in 2021.

They might be lying, and even if they aren’t, circumstances might change again before we get to next year. For now, things are going better than most expected. That’s good.

But what’s more interesting is that WeWork is finally making a turn towards what I recommended back in 2017. Before we get to that, let’s take a short coffee break.

Better Latte than Never

Over in Japan, Starbucks launched a new concept store that combines a coffee shop and a coworking space. As you can see in my tweet below, the first floor looks like a regular cafe, and the second floor includes cubicles and booths. These workstations can be booked in 40-minute increments on the spot or, in advance, on a dedicated web site.

.@Starbucks launches hybrid cafe-coworking space in Japan.https://t.co/tyctbSuazl pic.twitter.com/BGW1kt33sP

— Dror Poleg (@drorpoleg) August 3, 2020

Long-time readers know that I have long advocated for Starbucks to embrace the fact that many people come to its stores to work (and use the bathroom), rather than sip coffee. But that’s not why I’m bringing it up.

Starbucks’ experiment highlights an important point: People can work from anywhere and, sometimes, that anywhere is operated by a well-capitalized company that knows how to provide excellent service, to develop customer-focused spaces, and to market these spaces to the relevant people. It’s also a good opportunity to note that Starbucks’s mobile payment app was, until recently, the most popular mobile payment app in the US — ahead of more specialized competitors such as PayPal, Venmo, and Apple Pay.

And in a world where people can work from anywhere, a few companies can’t have a monopoly over the best places to work. But a single company can aggregate thousands of different spaces under a single digital platform.

Which brings us back to Airbnb and WeWork.

Never Get High On Your Own Supply

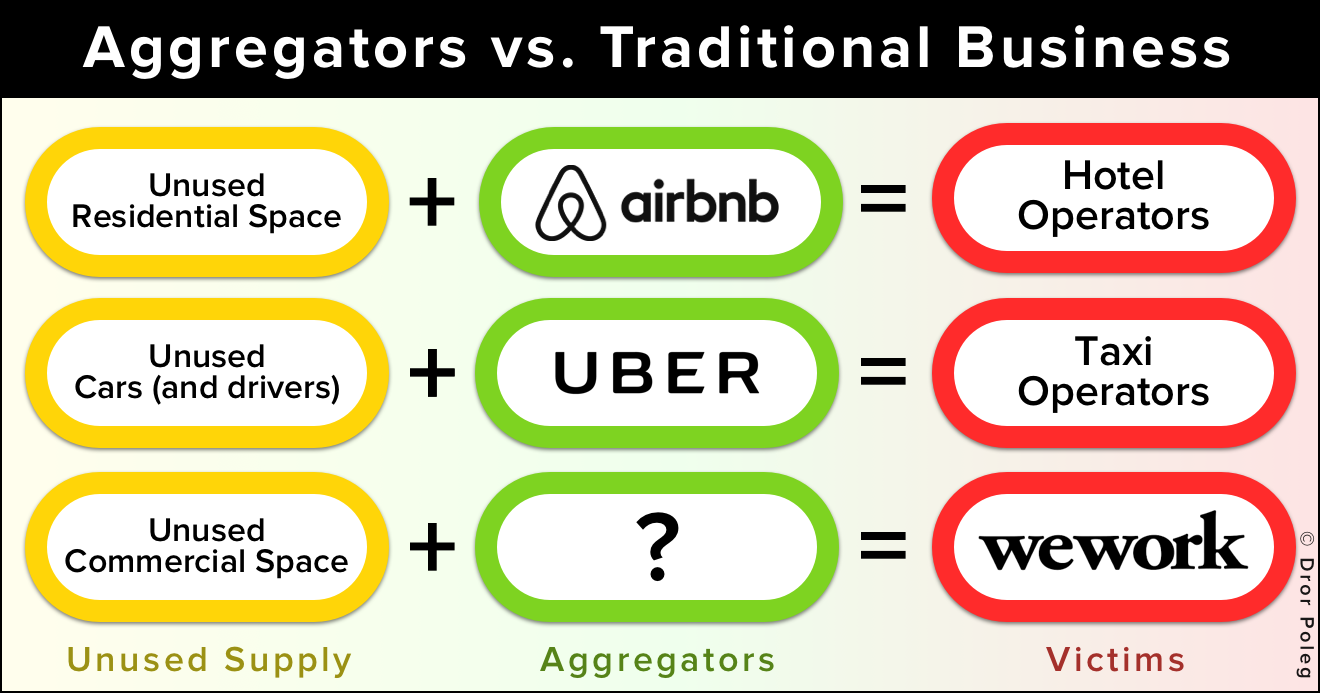

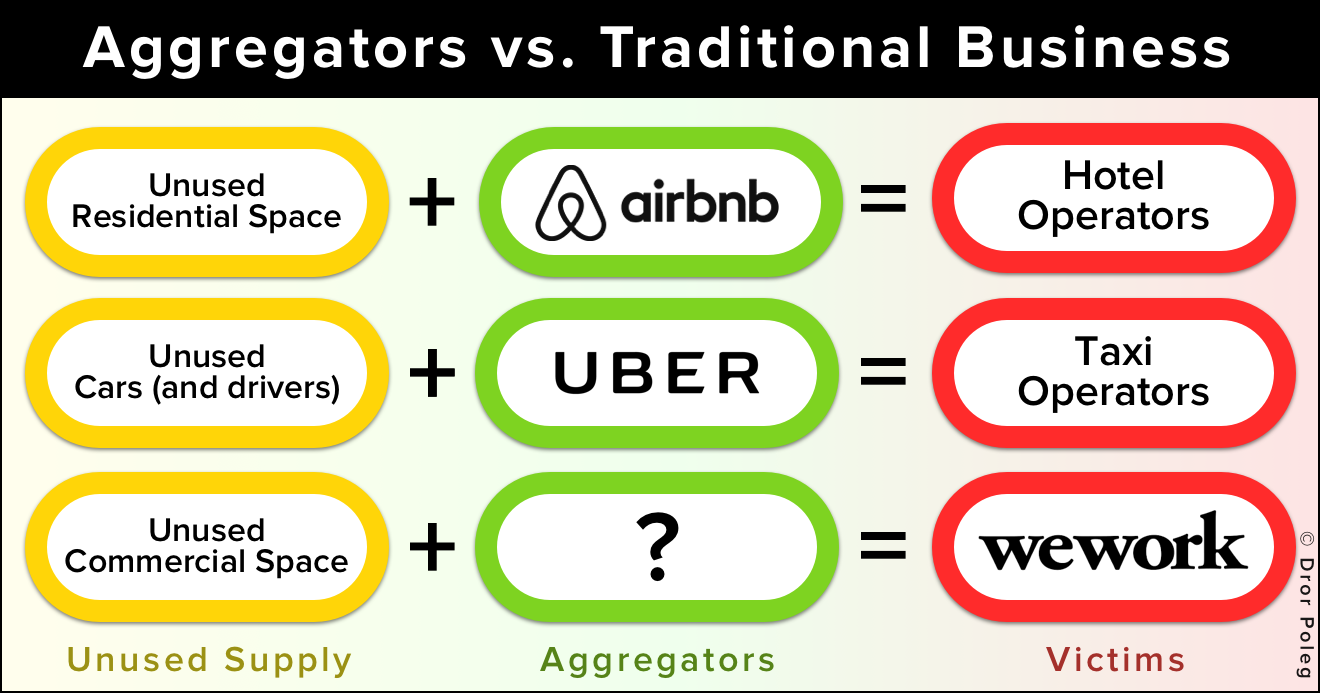

My 2017 article mentioned Airbnb to point out the weakness in WeWork’s model:

At its core, WeWork is in the business of developing supply and generating demand for its own spaces. Airbnb, in contrast, is in the business of aggregating existing supply and monopolizing demand for anyone’s spaces.

In other words, Airbnb is an aggregator of under-utilized spaces it does not own and does not have to pay fixed rent for. WeWork, on the other hand, relies on leases.

WeWork is now starting to move away from such leases. Instead, it is looking to forge more partnerships with landlords and, in some cases, to partner with investors to buy whole buildings. This would indeed help WeWork reduce the risk of its original model. That’s good.

But it’s no longer enough. WeWork is still built as a layer on top of the old world. That world assumed that, in each city, people only work in a few specific areas (business districts) and within a few particular types of buildings (office buildings). That world is dying.

In the new world, people spend much more time working across the whole city (and country) and within buildings that were not designed for office work — including hotels, cafes, repurposed street retail, homes, residential lobbies, even cars.

The world of workspaces (previously called offices) is becoming much more fragmented. Manhattan has less than five-hundred office buildings; it has about forty-three-thousand buildings. What happens when thousands of these buildings are suddenly potential workspaces?

In such a world, the leading brand is not likely to be a company that owns (or leases) spaces. The leading company in such a fragmented market is much more likely to be an aggregator — a digital destination where anyone can book a place to work, any time, for as long as they need it. And by “work” I also include activities that require access to specialized equipment such as podcasting, video production, light manufacturing, and more.

WeWork On Demand is a tiny step. For now, it only lists WeWork’s own locations. But if WeWork can grow it into an app that people use regularly, it could gradually add more spaces and turn it into the go-to destination for anyone who needs a place to work, anywhere. These spaces will not have to be leased or even operated by WeWork, just like Airbnb’s spaces are not leased or operated by Airbnb.

This is my vision for WeWork in the 21st Century. The company is very far from realizing this vision, but it is still in a better position to do so than any company on earth.

This last line also explains my increased optimism for Airbnb.

Eating a Bigger Pie

A year ago, I summarized my pessimism for Airbnb:

{kind=link}

As an aggregator, Airbnb aims to make a profit by monopolizing demand for shared housing. If all potential guests begin their journeys on the site, all the hosts will have to play by Airbnb’s rules (and pay Airbnb’s fees) in order to generate revenue from their properties. More than 250 million have already used Airbnb.

Fortunately, this makes it difficult (and very costly) for a new player to emerge and undercut Airbnb’s relationships with both hosts and travelers. Unfortunately, Airbnb is already swimming in waters infested with old players that are large, ruthless, and well capitalized.

Booking Holdings operates web sites such as Booking.com, Priceline, and Agoda.com. Expedia Group operates web sites such as as Hotels.com, Trivago.com, and Expedia.com. Marriott International operates thousands of hotels under brands such as Westin, W, Ritz-Carlton, St. Regis, Sheraton, and Marriott.

Together, these three companies generate about $10 billion in annual profits. Airbnb’a profit was $93 million in 2017 and recent reports indicate it is now losing money. Hosts and guests can easily shop around and use multiple platforms. This is particularly true for travelers who begin their journeys by searching on Google, another major player in the listings space.

And, indeed, Airbnb proceeded to lose money for a few quarters — even before COVID — and then see its valuation cut by 25% earlier this year. Everything I wrote about the company’s market and competitors is still valid.

So why am I more optimistic now?

Because Airbnb is moving away from that market. It is moving into a market that is much bigger, much more fragmented, and does not have ruthless and well-capitalized digital competitors. Airbnb is shifting its focus from the market for short stays to the market for long stays. It is no longer looking to be a flimsier or more authentic version of Marriott; it is looking to streamline the housing rental market.

That’s an ambitious goal. And, like WeWork, Airbnb is very far from realizing this vision, but it is still in a better position to do so than any company on earth.

Both WeWork and Airbnb have a long way to go. They might see their valuations cut once more. They might launch some failed initiatives. But the world is moving in their direction.

When people can live or work anywhere, they have to begin their journey somewhere. That “somewhere” will be a digital platform that makes it easy to find and book your next destination. This is already par for the course in the world of hotels. It is now coming to offices and homes. Are you ready?

{kind=link}

Old/New by Dror Poleg Newsletter

Join the newsletter to receive the latest updates in your inbox.